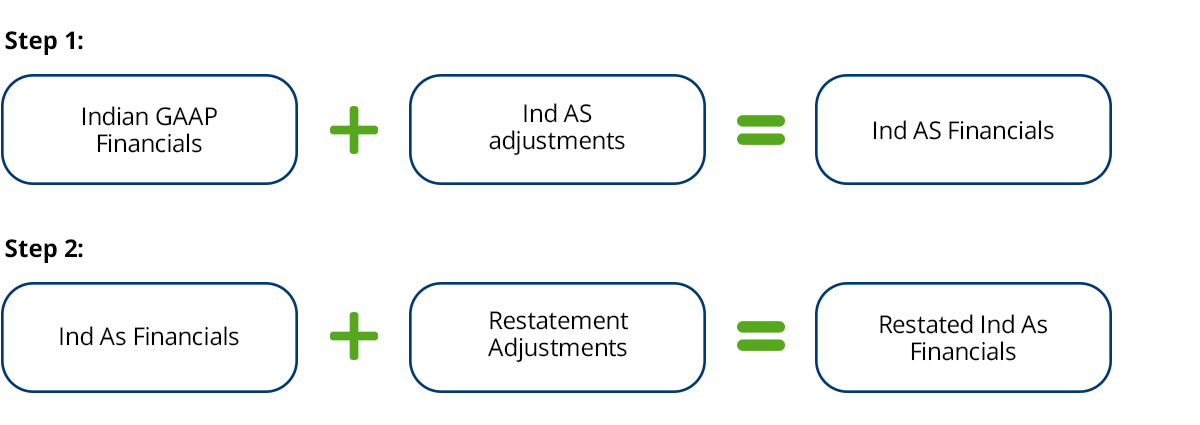

In the previous blog of the series on IPO reporting, we evaluated about the accounting framework applicable for the IPO. Accordingly, issuer company shall prepare restated consolidated financial information to be presented in the offer document based on reporting framework in which they have prepared their latest financial statements before filing offer document. Even if the latest financial statements are in Indian GAAP, SEBI has provided an option to issuer company to adopt Ind AS to restate the financial statements for all three years. Per our view, issuer company shall opt for the Ind AS reporting framework for the restated financial statements as it reduces time, costs, and efforts of the Company. Company could execute Ind AS restatement as well as IPO restatement at the same time by removing duplication of efforts which otherwise would be performed at different times.

In this blog, we will analyse the nature of adjustments required to prepare ‘Consolidated restated financial statements.

I. Restatement process.

There are two types of situations that may arise while restating the financials for IPO.

- Issuer Company was reporting under Ind AS prior to filing of DRHP.

- Issuer Company was reporting under Indian GAAP prior to filing of DRHP and will converge to Ind AS.

Situation A –Issuer Company was reporting under Ind AS prior to filing of DRHP

An issuer who is already preparing Ind AS compliant financial statements at the time of filing of DRHP is required to make only restatement adjustments as per ICDR regulations.

Situation B –Issuer Company was reporting under Indian GAAP prior to filing of DRHP and will converge to Ind AS

As per SEBI ICDR Regulations, 2018, an issuer can file restated financial statements as per Indian GAAP. However, the issuer will be covered under the Ind AS roadmap once the process of listing is started.

As per SEBI ICDR Regulations, 2018, an issuer can file restated financial statements as per Indian GAAP. However, the issuer will be covered under the Ind AS roadmap once the process of listing is started.

According to Ind AS, the companies are required to present a three-years balance sheet as per the requirements of Ind AS 101, First-time Adoption of Indian Accounting Standards. Thus, in our view, it is beneficial for the companies to voluntarily adopt Ind AS well in advance and prepare restated financial statements under Ind AS to avoid duplication of efforts. Apart from avoiding duplication, other benefits of early adoption of Ind AS are mentioned below:

- Certain Ind AS adjustments have an impact on the profitability as well as net worth (equity) of the company. This may have an impact on company valuation which is vital for IPO.

- Promoters and other stakeholders are aware well in advance of the impacts arising due to adoption of Ind AS before an IPO.

- Ind AS financials enhances credibility of the Company from the perspective of the future investors.

- It facilitates comparison of company’s performance with its peers/competitors.

II. Restatement adjustments

As per SEBI (ICDR) Regulations, 2018, the financial information should be restated to ensure consistency in the presentation, disclosures, and the accounting policies for all the periods presented in line with that of the latest financial year/stub period. Thus, the financial statements are required to be restated or adjusted for:

- change in accounting policies,

- incorrect accounting practices or failure to make provisions or for other significant errors and regrouping,

- change in accounting estimates,

- qualified opinion, adverse opinion, disclaimer of opinion

I. Change in accounting policies

As per ICDR Regulations, where there has been a change in the accounting policy, the profits or losses of the earlier years (forming part of restated financial information) and of the year in which the change in accounting policy has taken place should be recomputed to reflect the profits or losses of those years that would have been if a uniform accounting policy was followed in each of these years.

Examples, where restatement is required because of change in accounting policies, include introduction of new accounting standard, significant amendments in the existing standards, changes in the regulatory requirements, etc.

It is likely that the company would have changed accounting policies to comply with several of the accounting Standards or amendments that have become mandatory in the recent past.

Certain standards or amendments are applicable from a ‘particular date’ and may have ‘transitional provisions’ for executing such change. Such ‘applicability date for accounting standards or amendments would not be relevant since the company is adopting Ind AS for the first time. Thus, an accounting standard or amendments would have to be adopted throughout the period covered for the preparation of restated financial information. For e.g. Ind AS 115 – Revenue from contracts with customer and Ind AS 116 – Leases can be applied retrospectively. However, hedge accounting for which retrospective restatement is not allowed as per Ind AS 109, will applied prospectively.

II. Incorrect accounting practices or failure to make provisions or for other significant errors and regrouping:

Prior period errors are omissions from, and misstatements in, the company’s financial statements for one or more prior periods arising from a failure to use, or misuse of, reliable information that:

- was available when financial statements for those periods were approved for issue; and

- could reasonably be expected to have been obtained and considered in the preparation and presentation of those financial statements.

Such errors include the effects of mathematical mistakes, mistakes in applying accounting policies, oversights or misinterpretations of facts, and fraud. Regrouping of any financial item will have same accounting treatment to that of errors in restated financial statements.

If there is any prior period error in any of the years restated, the impact of the error needs to be reflected in the year it belongs to or the earliest period restated, whichever is later.

Examples, where restatement is required because of prior period errors, are:

- Incorrect accrual of expenses of the previous years accounted in the current year.

- Incorrect classification of expenses i.e., capital or operating in nature.

- Incorrect accounting of revenue

- Incorrect accounting of prepaid expenses

III. Change in accounting estimates

A change in accounting estimate is an adjustment of the carrying amount of an asset or a liability or the amount of the periodic consumption of an asset, that results from the assessment of the present status of, and expected future benefits and obligations associated with assets and liabilities. Changes in accounting estimates result from new information or new developments and, accordingly, are not corrections of errors.

The effect of change in an accounting estimate shall be recognised prospectively by including it in profit or loss in:

- the period of the change affects that period only; or

- the period of the change and future periods, if the change affects both.

In cases where the accounting estimate gives rise to changes in assets and liabilities or relates to an item of equity, it shall be recognised by adjusting the carrying amount of the related asset, liability or equity item in the period of the change.

Examples of changes in estimates are:

- Change in useful lives of depreciable assets

- Change in expected pattern of consumption of the future economic benefits embodied in depreciable assets

- Change in fair value of financial assets or financial liabilities

- Inventory obsolescence

- Bad debts

IV. Qualified opinion, adverse opinion, disclaimer of opinion:

Companies needs to assess any item qualified in auditor’s report and report under the Companies (Auditor’s Report) Order, 2016, as amended (including the Orders applicable for previous periods) for the periods covered by the restated financial statements in accordance with the principles enumerated in Ind AS 8, Accounting Policies, Changes in Accounting Estimates and Errors.

Companies should explain the adjustments made in the Restated Financial Information in relation to the items qualified in auditor’s report and the report under the Companies (Auditor’s Report) Order, 2016, as amended (including the Orders applicable for previous periods) in the notes to Restated Financial Information.

SEBI ICDR regulations require the restated financial statements to incorporate adjustments with respect to all the errors and misstatements that were identified to the maximum extent possible in the years it pertains to, or the earliest period restated, whichever is later. Even when the incorrect practices or errors are nonquantifiable, companies are required to appropriately disclose the same in the notes along with an explanation as to why the qualification cannot be quantified or estimated.

Summary

As per SEBI (ICDR) Regulations, 2018, it is necessary for an issuer company to prepare the restated consolidated financial information considering above adjustments as per Schedule III to the Companies Act, 2013 for a period of three financials years and for the stub period (if any) in tabular form. The restated financial information shall be audited and certified by the statutory auditors who holds a valid certificate issued by the Peer Review Board of the Institute of Chartered Accountants of India (ICAI). Generally, a company would require a minimum six to nine months to compile restated consolidated financial information. Considering the time and challenges involved, the restatement process is extremely critical milestone for a company preparing for an IPO.

We, at FinPro Consulting, assist many of our clients for preparing restated consolidated financial information for an IPO purpose. We advise and assist companies on when to adopt Ind AS while going for an IPO, how to prepare restated financial statement for DRHP / RHP / Prospectus, drafting Employee Stock Option (ESOP) Schemes, etc. We have resources with extensive experience in Ind AS Convergence, IPO restatements, etc. and thus we can provide deep insights on the path of an IPO.