Cart 0

Introduction

Share-based payment (SBP) plans have become increasingly common and form an important component of the total employee compensation package. Share purchase plans and share option plans are a popular feature of employee remuneration, for directors, senior executives and many other employees. Under Indian generally accepted accounting principles (GAAP), the Guidance Note on ‘Accounting for share-based payments (Revised 2020)’ issued by the Institute of Chartered Accountants of India (ICAI) establishes financial accounting and reporting principles for share-based payments. Under Ind AS / IFRS, accounting of these share-based payment transactions is covered by Ind AS 102 / IFRS 2. Proposed accounting treatment under Indian GAAP for SBP transactions by way of an exposure draft of AS 102 – Share-based Payments is also prescribed on similar principles.

Share-based payments are not only restricted to an entity’s own share options but can also extend to the transactions involving the share options of another group entity (commonly known as “group share-based payment”). It is common for employees of an entity to receive share options or rights to subscribe to shares of another entity within the group, generally that of the parent’s shares. For example, within a multinational group, share options of the listed parent entity may be granted to the employees of various subsidiaries located in different countries across the world.

In this blog, we will get an overview of accounting requirements for the group-SBP arrangements in the financial statements of the parent, subsidiary, and in the consolidated financial statements of a parent entity.

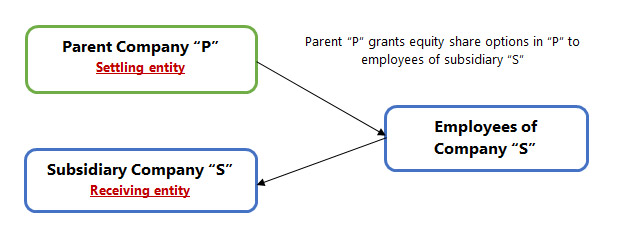

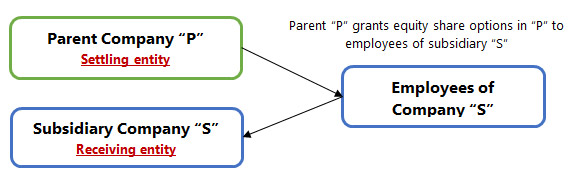

What is group-SBP arrangement?

In the above scenario, employees of a subsidiary company “S” are granted share options of its parent entity “P” for services provided to the subsidiary company “S”. Similarly, employees of subsidiary “S” may be granted cash payment based on the fair value of equity shares of parent “P”. Parent P is not the reporting entity when S prepares its financial statements. Share-based payment arrangements involve entities other than the reporting entity however, entities within the group are referred to as ‘group share-based payment’, these may be equity-settled or cash-settled SBP transactions.

The relevant entities in a group share-based payment transaction are described as:

- a ‘receiving entity’ is the entity that receives goods or services in a share-based payment transaction; and

- a ‘settling entity’ is the entity that has the obligation to settle the share-based payment transaction.

How to account for a group SBP arrangement?

SBP transaction is required to be accounted for in the books of both receiving and settling entity as well as in the consolidated financial statements of the parent entity. Accounting for group share based payment transactions will depend on whether arrangement is equity settled or cash settled i.e., classification and whether expenses will be rechargeable from the receiving company or not.

IFRS 2 / Ind AS 102 – Share based payments, provides a clear basis to determine the classification of awards in both consolidated and separate financial statements by setting out the circumstances in which group share-based payment transactions are treated as equity-settled and cash-settled. The amount recognised by the receiving entity may not necessarily be consistent with the amount recognised in the consolidated financial statements.

Classification of SBP transaction in the books of receiving entity

The entity receiving the goods or services should account for awards as equity-settled by debiting share-based payment expenditure and crediting equity when entity has either:

![]()

In all other circumstances the receiving entity classifies a group share-based payment transaction as cash-settled for e.g. if it has an obligation to settle in cash or other assets. ‘Other assets’ include the equity instruments of another group entity, in the separate financial statements of the receiving entity.

Classification of SBP transactions in the books of settling entity

A settling entity classifies a share-based payment transaction as equity-settled if and only if it settles the transaction in its own equity instruments. Otherwise, it classifies the transaction as cash-settled.

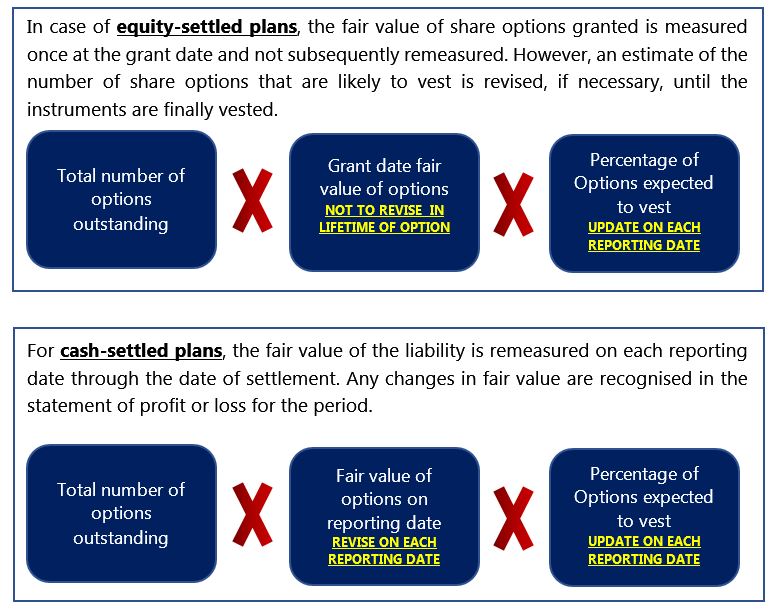

Subsequent accounting i.e. the recognition and measurement of the share-based payment transaction depends on the classification of the transaction between equity-settled share-based payments or cash-settled share-based payments.

Kindly refer Annexure 1 for further details on the classification of SBP transactions within the group.

Measurement of SBP transactions:

Total share-based payment expenditure to be recognised over the vesting period in case of both equity settled and cash settled transaction is calculated as below:

What is a recharge arrangement?

Certain group share-based payment arrangements include a recharge where the parent entity charges the subsidiary for the equity or cash it provides to the employees (or other providers of goods or services) of the subsidiary. Though this scenario is not specifically addressed under IFRS 2 / Ind AS 102 or any of the related guidance, an appropriate view could be that so long as there is a clear link between the recharge and the share-based payment, it may be appropriate to offset the recharge against the capital contribution in the separate financial statements of the subsidiary and the parent entity.

Existence of a recharge arrangement between the settling entity and the receiving entity does not change the character of the share-based payment transaction, and therefore would not affect the classification of the share-based payment transaction as equity-settled or cash-settled.

Accounting in the separate financial statements of receiving entity, settling entity and consolidated financial statements of settling entity:

Continuing with our original illustration:

-

Accounting in the separate financial statements of “S” (Receiving entity)

S, as the receiving entity, has no obligation to settle the transaction with the counterparty to the SBP transaction, recognises ‘SBP expense’ for the goods or services received from the counter party, unless the goods or services received qualify for recognition as an asset. In case recharge arrangement, equivalent credit will be accounted as ‘Payables’ to parent, otherwise in case of absence of recharge, ‘Equity contribution by the parent’. Amount is measured equivalent to the proportionate share of total SBP expense to the period lapsed.

| Books of Subsidiary S (Receiving entity) (SFS) | |

|---|---|

| Debit | SBP Expense A/c. |

| Credit | Payable A/c. (In case of recharge arrangement) OR Equity contribution by Parent A/c. |

-

Accounting in the separate financial statements of “P” (Settling entity)

P, as the settling entity, accounts for the transaction as equity-settled if it has an obligation to settle the transaction in its own equity instruments. In case of recharge arrangement, debit will be accounted as ‘Receivables’, otherwise in absence of recharge, ‘Investment in the subsidiary’ Corresponding credit will be accounted as ‘Equity SBP Reserve’ in case of equity SBP transaction or ‘SBP Liability’ in case of cash settled SBP transaction.

| Books of Parent P (Settling entity) (SFS) | |

|---|---|

| Debit | Receivable A/c. (In case of recharge arrangement) OR Investment in Subsidiary A/c. |

| Credit | Equity SBP Reserve A/c. (Equity settled) |

-

Accounting in the consolidated financial statements of “P” (Settling entity)

P accounts for the transaction as equity-settled in its consolidated financial statements, since, from the perspective of P Group, it has an obligation to settle in its own equity instruments.

| Books of Parent P (Settling entity) (CFS) | |

|---|---|

| Debit | Equity SBP Expense A/c |

| Credit | Equity SBP Reserve A/c. (Equity settled) |

What if employees transfer within the group?

In some circumstances, a Parent may grant options to the employees that are conditional upon employee providing the service within the Group than restricting it to one particular entity. In such circumstances, the options shall still vest with the employee on transfer from one entity to another within the Group.

The subsidiary receiving the goods or services shall account for the awards as equity-settled where it has no obligation to settle the share-based payment transaction. Each subsidiary measures the services received from the employee with reference to the parent’s grant-date fair value of the equity instruments and recognises the corresponding SBP expenses. Where the employee is transferred to another entity within the Group; the employee compensation expenditure is adjusted on cumulative basis in the respective financial year.

For example, Parent P grants 100 options over its own equity shares to an employee with 3 years’ service condition within the group i.e. if employee stays within the group for at least 3 years, options will vest to him. Entities X1, X2 and X3 are part of the P’s group. Employee is initially employed in X1, and P grants him equity option to be vested after 3 years. The grant-date fair value of an option is INR 9.

-

Accounting entry in books of Parent P for year 1:

| Debit | Investment in Subsidiary X1 [(100 X INR 9 X 100%) X 1/3] |

300 |

|---|---|---|

| Credit | Equity SBP Reserve A/c (Equity settled) | 300 |

-

Accounting entry in books of Subsidiary X1 for year 1:

| Debit | SBP Expense A/c | 300 |

|---|---|---|

| Credit | Equity A/c (contribution from Parent) | 300 |

During Year 2, employee was shifted from entity X1 to entity X2.

-

Accounting entry in books of P:

| Debit | Investment in Subsidiary X2 | 300 |

|---|---|---|

| Credit | Equity SBP Reserve A/c (Equity settled) | 300 |

In Year 2 – i.e. when the employee leaves X1 – X1 does not adjust any previous entries, nor does it recognise any further expenses.

-

Accounting entry in books of X2:

| Debit | SBP Expense A/c | 300 |

|---|---|---|

| Credit | Equity A/c (contribution from Parent) | 300 |

X2 does not recognise any catch-up on for the cumulative expenses to date, because Year 1 expenses have already been recognised by X1.

Summary

It is common for employees of an entity to receive shares options or rights to shares in another entity within the group. Receiving and settling entities will have to record a share-based payment expense transaction in their separate as well as consolidated financial statements, irrespective of whether there is any recharge from the group company or not. Its accounting is dependent on the classification of the SBP transaction, whether equity-settled or cash-settled. Please refer to Annexure 1 below in order to evaluate the classification of group SBP transactions.

Annexure 1 – Classification of SBP transaction in case of Group SBP transactions

The scenario assumes P as the parent Company; S as the subsidiary Company and services of employees are received by the Company S.

| Sr. no. | Obligation entered by | Share options in | Classification of share-based payments | Remarks | ||

|---|---|---|---|---|---|---|

| In FS of “P” | In FS of “S” | In CFS of “P” | ||||

| 1 | Company P | Company P | Equity-settled | Equity-settled | Equity-settled | The share options are for shares in “P” and obligation is entered by P, therefore equity-settled in FS of “P”. “S” does not have obligation to settle, hence the options are recognised as equity-settled in FS of “S”. In CFS, the options are equity-settled since options are for shares in “P”. |

| 2 | Company P | Company S | Cash-settled | Equity-settled | Equity-Settled | The share options are for shares in “S”, & obligation is entered by P; therefore cash-settled in FS of “P”. “S” does not have obligation to settle, hence the options are recognised as equity-settled in FS of “S”. In CFS, the options are equity-settled since options are for shares in “S”. |

| 3 | Company S | Company P | — | Cash-settled | Equity-Settled | No obligation is entered by P; therefore, no impact in P’s FS. The share options are for shares in “P”; therefore, cash settled in FS of “S”. In CFS, the options are equity-settled since options are for shares in Group. |

| 4 | Company S | Company S | — | Equity-settled | Equity-Settled | No obligation is entered by P; therefore, no impact in P’s FS. The share options are for shares in “S”; therefore, equity settled in FS of “S”. In CFS, the options are equity-settled since options are for shares in Group. |

| 5 | Company P | Cash based on P’s shares | Cash-settled | Equity-settled | Cash-Settled | “S” does not have obligation to settle, hence the options are recognised as equity-settled in FS of “S”. In CFS and FS of “P”, the options are cash-settled since obligation is to be settled in cash. |

| 6 | Company P | Cash based on S’s shares | Cash-settled | Equity-settled | Cash-Settled | “S” does not have obligation to settle, hence the options are recognised as equity-settled in FS of “S”. In CFS and FS of “P”, the options are cash-settled since obligation is to be settled in cash. |

| 7 | Company S | Cash based on P’s shares | — | Cash-Settled | Cash-Settled | No obligation is entered by P; therefore, no impact in P’s FS. In CFS and FS of “S”, the options are cash-settled since obligation is to be settled in cash. |

| 8 | Company S | Cash based on S’s shares | — | Cash-Settled | Cash-Settled | No obligation is entered by P; therefore, no impact in P’s FS. In CFS and FS of “S”, the options are cash-settled since obligation is to be settled in cash. |

We, at FinPro Consulting, assist many of our clients for preparing and drafting ESOP schemes, valuation of options and accounting and disclosures for the SBP transactions. We advise and assist companies on how and when to issue ESOPs to the employees, and also maintain a dialogue with the merchant bankers. We have resources with extensive experience in valuation of ESOP and other financial assets, Ind AS Convergence, IPO restatements, etc. and thus we can provide deep insights to the our clients on this path.

5,960 Views