Cart 0

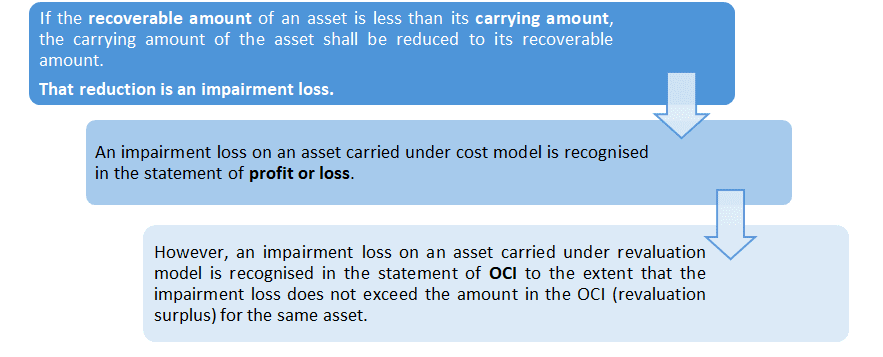

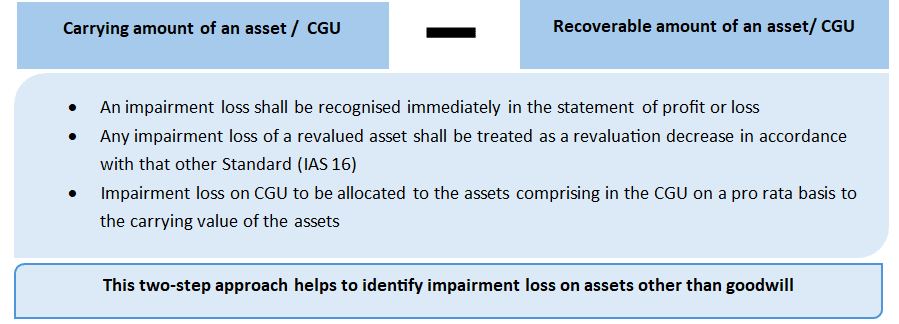

In our previous blogs, as a part of IAS 36- Impairment of Assets, we discussed on what is cash generating unit (CGU), recoverable value, value in use and how to calculate impairment loss etc. Impairment loss is calculated as carrying value of an asset or CGU less its recoverable value.

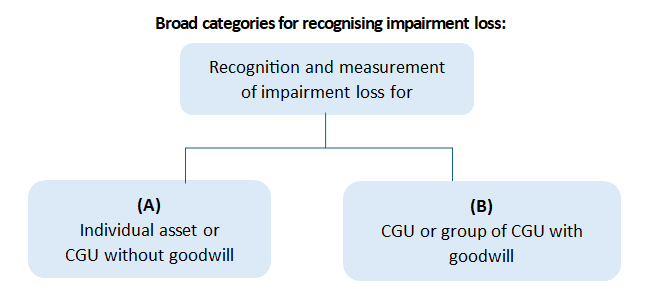

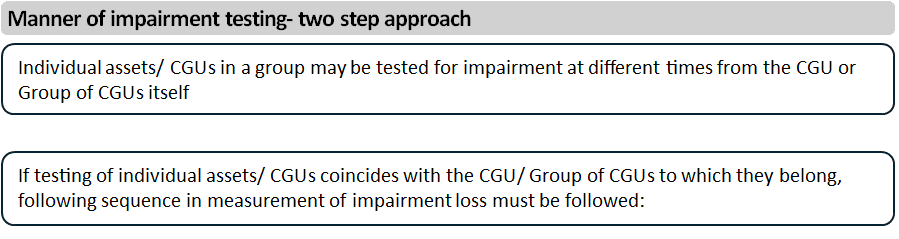

In this blog we will further discuss how to recognise and measure impairment loss of individual asset or CGU or group of CGU, whether with and without goodwill. Accounting entries for impairment loss on assets or CGU is provided for easy understanding. We’ll also discuss the manner of impairment testing to be followed if testing of individual assets/ CGUs coincides with the CGU/ Group of CGUs to which they belong.

Recognising and measuring impairment loss

(A) Individual asset or CGU without goodwill

Accounting entry:

|

Statement of P&L / OCI (in case of revalued assets) A/c Dr. (Impairment loss, if any on individual asset or CGU without goodwill) |

XXX | |

| To Individual Asset or asset under CGU in proportion to their CV | XXX |

- After the recognition of an impairment loss, the depreciation (amortisation) charge for the asset shall be adjusted in future periods to allocate the asset's revised carrying amount over its remaining useful life;

- If an impairment loss is recognised, any related deferred tax assets or liabilities are determined in accordance with IAS 12

- The word “asset” used while calculating the impairment loss shall also include “cash generating unit”

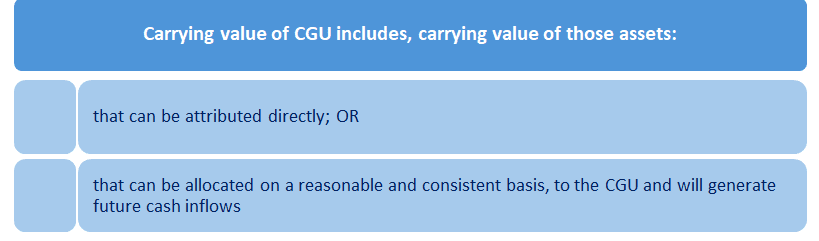

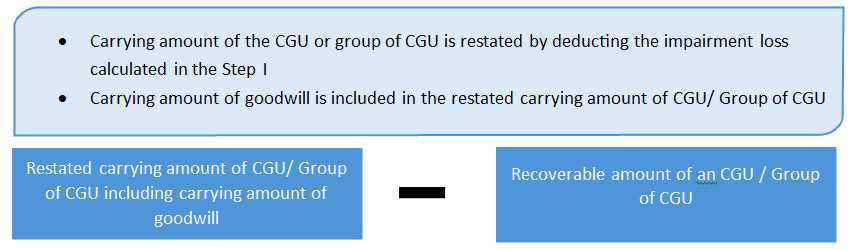

Carrying value of CGU:

Carrying value of CGU does not include the carrying amount of any recognised liability, unless the recoverable amount of the cash-generating unit cannot be determined without consideration of this liability.

(B) Impairment loss for CGU or group of CGU with goodwill

Allocation of goodwill on CGU or group of CGUs:

- Goodwill acquired in the business combination to be allocated on all the CGUs or group of CGUs;

- That are expected to benefit from the synergies or combination;

- Irrespective of whether other assets of acquiree are assigned to those CGUs or group of CGUs

- Each unit or group of units to which the goodwill is so allocated will represent the lowest level within the entity and level shall not be larger than an operating segment

- Management may monitor the goodwill at a broader level than the other assets. Thus, there may be few CGUs to which goodwill is attributable but has not been allocated because the goodwill has been allocated to the larger CGU to which it is a part.

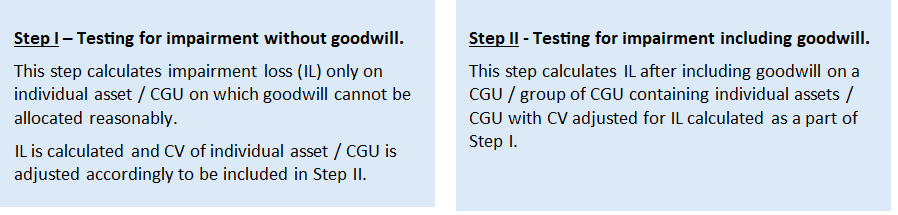

Step I – Individual assets or CGU without allocated goodwill

Accounting entry:

|

Statement of P&L / OCI (in case of revalued assets) A/c.

Dr. (Impairment loss, if any on CGU without goodwill) |

XXX | |

| To Assets under CGU in proportion to their CV | XXX |

Step II – Impairment loss CGU or group of CGUs with allocated goodwill

- An impairment loss shall be recognised immediately in profit or loss / OCI.

- Impairment loss on CGUs / Group of CGU to be allocated as below:

- first to reduce any carrying amount of goodwill allocated; and then

- to other assets of CGU/ Group of CGU on a pro rata basis to the carrying value of the asset

Accounting entry:

|

Statement of P&L / OCI (in case of revalued assets) A/c.

Dr. (Impairment loss, if any on CGU without goodwill) |

XXX | |

| To Goodwill (Allocated on CGU) | XXX |

|

| To Assets under CGU in proportion to their CV (Remaining IL after reducing Goodwill to zero) | XXX |

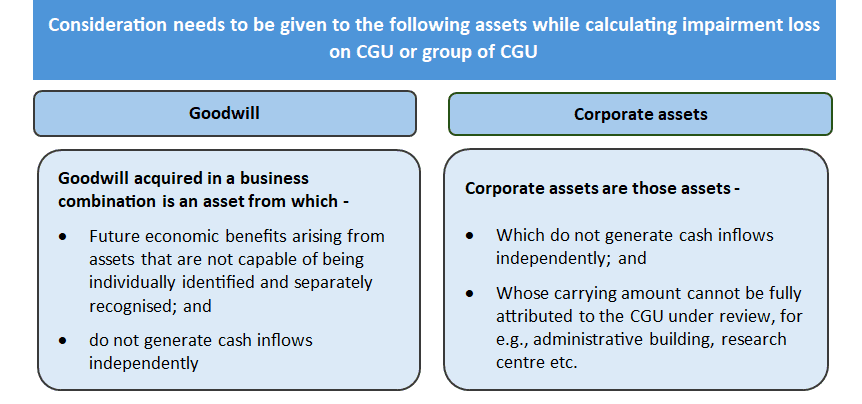

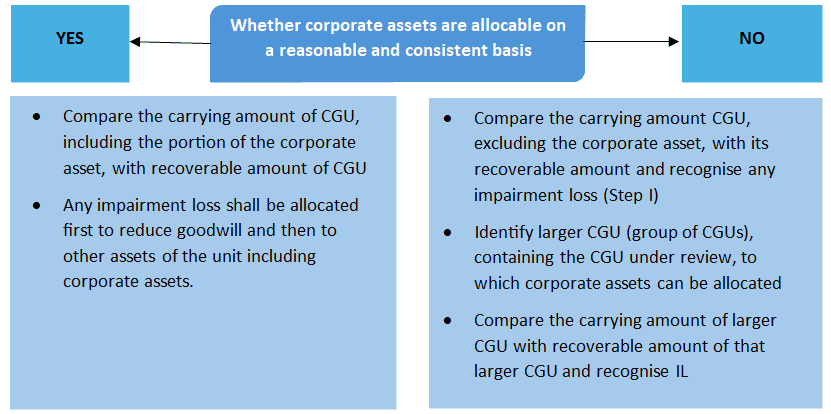

How to consider corporate assets in impairment testing?

We hope this blog helps to understand how to recognise and measure impairment loss of individual asset/ CGU or group of CGUs. Goodwill or corporate assets does not independently contribute towards generating cash inflow, thus slightly different approach required to be followed while measuring impairment loss for corporate assets and CGU or group of CGUs with allocated goodwill.

Thank you for reading this article. Stay tuned for more simplified insights on accounting standards!

About the Author:

This blog is part of our ongoing effort to simplify complex IFRS topics for learners and professionals. To dive deeper into IAS 36 and other IFRS standards, enroll in our ACCA DipIFR online course designed for finance professionals across India and abroad.

63 Views